B-SOFT CO. LTD.(300451)OUTLINES OF IN-DEPTH ANALYSIS:WITH FAVORABLE ENVIRONMENTS NEW PROSPERITY UNDERWAY

Company Profile B-Soft Co., Ltd. is a China-based company principally involved in medical and health information construction. It operates three businesses. The medical and informatization application software business includes hospital information application software and public health information application software. The information technology-based system integration business includes computer information equipment system integration business and intelligent network cabling engineering integration business. The information technology (IT) operation and maintenance service business includes financial self-service equipment professional technical service business and medical industry's maintenance technology service business. The Company mainly conducts its businesses in domestic market. (Source: MarketScreener) Investment Highlights As a leading player of medical and health information construction, B-Soft Co., Ltd. (“B-Soft”/ the company) maintains a strong impetus for steady growth. Established in 1997, based on the business strategy of “one body and two swings”, the company, taking medical and informatization application software business, its conventional business, as a cornerstone, has expanded its business to IT-based system integration and intelligence innovation. As a leading player of medical and informatization construction, B-Soft, benefited from the continuous expansion of demand, has demonstrated a decent growth in its past performance, with the CAGR of revenue and net profit from 2017 to 2021reaching 13.29% and 26.27%, respectively. Meanwhile, the company has continued to better its equity structure to build an ecosystem of great health. In May of 2022, Philips became its second largest shareholder, with a 10% stake in the company. The company’s medical and informatization application software business, its conventional business as well as its cornerstone, will embrace a comprehensive growth. Thanks to the continuous catalyst of favorable policies and the post-epidemic era, the demand is expected to recover. And the medical and health information construction will also bring in new demand. 1) As for hospitals, the company has developed capabilities with “one-stop” solutions, and has been working on the core software for years including HIS, CIS. 2) As for public health, the company, complying with industrial policies and taking clients’ demand into consideration, has promoted the connectivity of information and continued to explore new business modes. 3) In terms of medical insurance, with the platforms for medical insurance becoming more available and the acceleration of DRG/DIP pilots, the company has grasped good development opportunities. The company has actively expanded its two swings. The information technology-based system integration and intelligent network cabling engineering integration are two innovative businesses to which it has attached great importance. 1) As for the IT-based system integration, the company has deepened cloud strategy and internet-based medical care strategy, promoted the implementation of its “cloud 2.0” strategy and the construction of its cloud ecosystem. And Hi-HIS is expected to bring in incremental revenue. 2) In terms of intelligent network cabling engineering integration, the company has expanded product and maintenance services of Internet of Things (IoT), and its 5G medical intelligent products co-developed with HUAWEI have been produced in mass. 3) The company will cooperate with Philip and deepen the synergy in channels and products. CTasy is expected to accelerate the market promotion in 2023. Earnings forecast and investment recommendation The company will continue to focus on the development of “one body two swings” to grasp opportunities in clouding, online development and medical insurance reforms. In the meantime, with the cooperation with Philip going deep, the synergy effect is expected to stand out. We revised our forecasts for its net income attributable to shareholders at CNY 53 million in 2022, CNY 450 million in 2023, and CNY 590 million in 2024. Maintain “Outperform”. Potential risks slower-than-expected deliveries and bid progress due to macroeconomic disruptions; slower-than-expected pilot promotion of health cities and medical insurance reforms; slower-than-expected application promotion of new technologies such as business clouding and intelligence

【免责声明】本文仅代表第三方观点,不代表和讯网立场。投资者据此操作,风险请自担。

【免责声明】本文仅代表第三方观点,不代表和讯网立场。投资者据此操作,风险请自担。

“B-SOFT CO. LTD.(300451)OUTLINES OF IN-DEPTH ANALYSIS:WITH FAVORABLE ENVIRONMENTS NEW PROSPERITY UNDERWAY” 的相关文章

调查显示欧元区消费者对未来12个月通胀预期上升

欧洲中央银行12月7日公布的10月欧元区消费者预期调查显示,相比9月,欧元区消费者对未来12个月的通胀预期进一步上升。 该项调查对象为比利时、德国、西班牙、法国、意大利和荷兰约1.4万名成年消...

{易七娛樂註冊}(林芝旅游景点大全排名)

今天给各位分享林芝旅游景点大全的知识,其中也会对林芝旅游景点大全排名进行解释,如果能碰巧解决你现在面临的问题,别忘了关注本站,现在开始吧!本文目录一览: 1、林芝旅游景点有哪些 这些地方打卡必备...

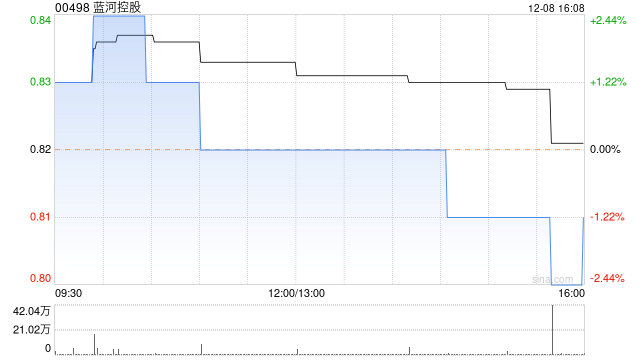

蓝河控股12月8日斥资约8万港元回购10万股

蓝河控股(00498)发布公告,该公司于2022年12月8日斥资约8万港元回购10万股,回购价为每股0.8港元。...

中信证券:首予商汤-W增持评级 目标价2.3港元

中信证券发布研究报告称,首予商汤-W(00020)“增持”评级,目标价2.3港元。公司为人工智能和计算机视觉行业龙头,独创“1基础研究+1产品解决方案+X行业”的商业模式,业务涵盖智慧商业、智慧...

{易七現金網}(西藏旅游必去景点推荐)

去西藏旅游需要注意以下几个方面要保证自己在进藏之前和旅游期间不要感冒,尤其是在十月份到第二面四月份之间,因为西藏高寒缺氧,感冒容易引发高原肺水肿,价值高原医疗条件一般,高原肺水肿不容易治疗,甚至会有生...

{易七現金網}(西北大环线旅游8天游攻略)

1、主要景点有鸬鹚潭进入峡谷的第一个景点此处为昔日鸬鹚鸟栖居之地,以山田大桥西侧的一汪清潭为主景,临潭的青羽岗受水流冲蚀,有千疮百孔之状岗顶有倚青枕白亭一座,沿岗顶拾给级而下至鸬鹚湾中有卧鸬石唤鸬。...